Lifecycle analysis shows key financial insights that many wastewater treatment facilities miss. A large study looking at 83 case studies of wastewater treatment’s life cycle costs points to an ongoing change. Treatment facilities are moving away from conventional cost analysis toward environmental life cycle cost analysis.

The numbers tell an interesting story. About 44% of these studies use different methods to combine lifecycle analysis with their assessments. A closer look at the economic picture shows that modern sewage treatment plants need less energy and fewer staff than older systems. On top of that, decentralized treatment setups cost less environmentally than centralized ones. However, centralized wastewater treatment plants tend to generate higher net cash flow per functional unit.

The money-saving benefits go well beyond day-to-day operations. Smart investments in sewage treatment technology mean treated water can be reused in landscaping, flushing, and industrial cooling. This is a big deal as it means that facilities can cut their water procurement costs. This piece will get into how life cycle cost analysis reveals hidden costs and savings. We’ll look at different analytical frameworks and practical ways to boost both environmental and financial results in wastewater infrastructure.

Defining Lifecycle Analysis in Wastewater Treatment

Lifecycle analysis offers a proven way to evaluate environmental impacts and benefits of processes or products from start to finish. Wastewater treatment facilities use this analytical framework to make smart decisions that protect the environment and manage costs.

Scope of lifecycle analysis assessment in WWT

Lifecycle assessment (LCA) in wastewater treatment looks at negative effects while meeting environmental regulations. This environmental tool studies the complete lifecycle of wastewater processes. The analysis starts from raw material acquisition and continues through use, end-of-life treatment, recycling, and final disposal. The International Organization for Standardization (ISO) lists four key steps to conduct a reliable and valid LCA through ISO 14040:2006 standards:

- Goal and scope definition – Establishing the functional unit, system boundaries, and analysis level

- Life cycle inventory (LCI) – Collecting necessary data for the study system

- Life cycle impact assessment (LCIA) – Gathering information and assessing environmental impacts

- Life cycle interpretation – Analyzing and discussing LCI and LCIA results

System boundaries in wastewater treatment LCA studies show big variations. A review of 35 published LCA studies from 2006 to 2022 revealed that 80% included sludge treatment and disposal. These stages were included because they affect the overall environmental impact. Only 7% of studies looked at the complete lifecycle from construction through disposal/demolition.

The functional unit (FU) measures the quantity flowing through the system. Most wastewater LCA studies use 1 m³ of treated wastewater as their functional unit. Some employ population equivalents (PE/year) instead. Rodriguez-Garcia’s study found that this choice affects how we interpret results. Global warming impacts and economic costs drop with better eutrophication treatment when using volume-based functional units.

Wastewater LCA typically measures energy consumption, greenhouse gas emissions, eutrophication, and toxicity. Global warming potential (GWP) ranks among the most calculated metrics. Studies also track acidification potential, ozone depletion potential, and photochemical ozone creation potential.

Difference between LCA and LCCA in wastewater systems

Life Cycle Assessment (LCA) and Life Cycle Cost Assessment (LCCA) serve different purposes in wastewater systems, despite their similar names.

LCA measures environmental impacts throughout a product or process’s life. LCCA calculates the total cost of ownership. The key difference is simple – LCA shows environmental impact while LCCA reveals total ownership cost.

LCCA considers net cash flow (revenues and expenditures) plus environmental costs for economic evaluation. This method helps find cost-effective options across different treatments. Advanced analyzes use net present value (NPV) calculations. NPV discounts future cash flows to determine if investments will be profitable.

LCCA comes in three main types. Conventional LCC focuses on direct costs. Environmental LCC includes monetized environmental impacts. Societal LCC adds broader social costs. Each type offers more detailed coverage of true lifecycle costs but becomes more complex.

Why lifecycle thinking matters in infrastructure planning

Lifecycle thinking goes beyond environmental assessment. It considers economic and social impacts throughout a product or service’s existence – from “cradle to grave”. This integrated approach proves valuable for wastewater infrastructure planning because decisions affect decades of operation.

Applying lifecycle thinking to wastewater treatment facility planning brings key benefits. It shows environmental trade-offs between treatment technologies. To name just one example, a study of sequential batch reactors (SBRs) and constructed wetlands revealed that SBRs had bigger environmental impacts because they used more electricity.

This analysis also spots “hotspots” – areas that create outsized environmental or economic impacts. The operational phase creates the biggest environmental impact, mostly through electricity used in treatment. Knowing these hotspots helps planners focus improvements where they matter most.

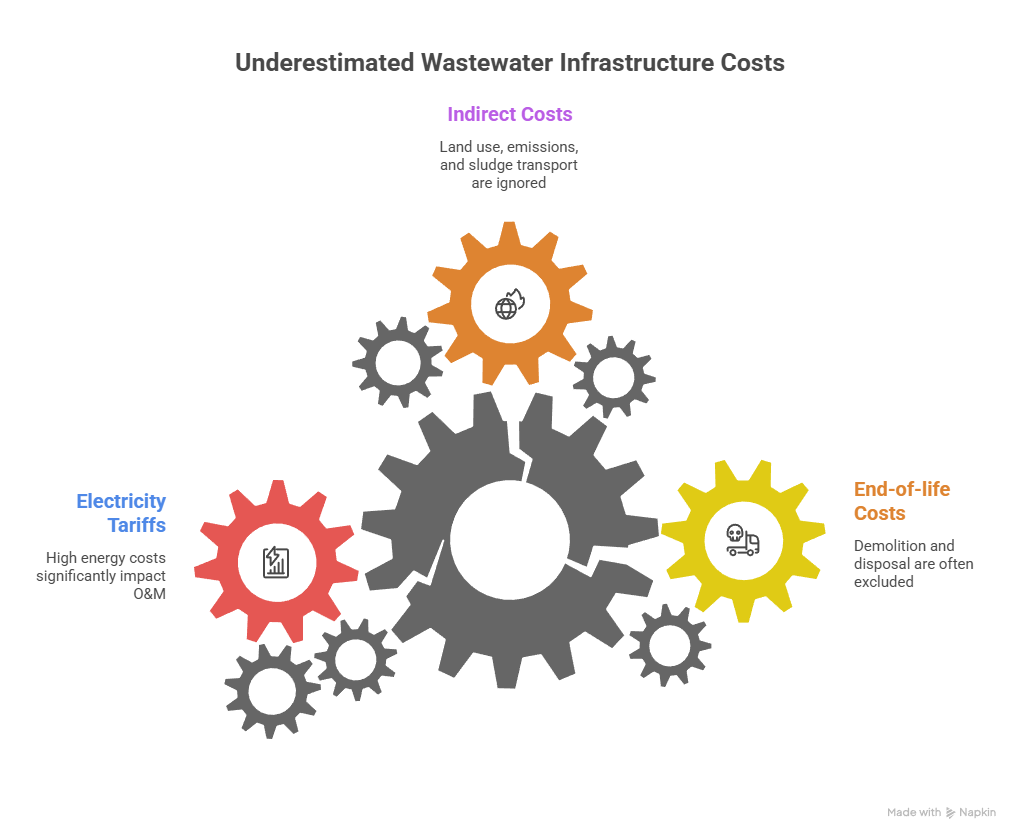

Lifecycle thinking leads to better long-term planning by including often-ignored costs. These costs include end-of-life expenses, demolition, and indirect costs like land use, emissions, and sludge transport. This detailed view results in resilient, sustainable infrastructure decisions that work for both the environment and finances.

Frameworks for Life Cycle Cost Analysis (LCCA)

A well-laid-out framework helps manage costs in wastewater treatment projects. This framework should track all expenses throughout a facility’s life. Life cycle cost analysis (LCCA) gives us several ways to assess financial, environmental, and social factors when planning infrastructure.

Conventional vs Environmental vs Societal LCC

The Society of Environmental Toxicology and Chemistry (SETAC) created a detailed classification system. Their system splits LCCA into three distinct categories that grow in scope and complexity.

Conventional LCC looks at traditional financial assessments of marketed goods and services. Companies use this approach when they care about their direct costs. It serves as the foundation for most financial analyzes but misses broader effects beyond immediate spending.

Environmental LCC builds on the basic approach. It lines up with the system boundaries used in lifecycle assessment (LCA). The method still looks at finances but covers costs that affect all stakeholders in the system. Environmental LCC connects traditional cost accounting with environmental factors to create an integrated evaluation framework.

Conventional LCC takes another step by putting a price tag on environmental and social effects. It uses accounting prices to measure these impacts. People call this a “socio-economic” or “welfare-economic” assessment. These three LCC types give us a clear system to evaluate economics, either with LCAs or on their own.

The frameworks show how cost profiles change based on wastewater makeup. A newer study about brine wastewater treatment systems found treatment costs between €10/m³ and €25/m³. The greenhouse gas emissions ranged from 10-17 kg CO₂e/m³. Both numbers dropped at full scale and changed with energy costs, chemical expenses, and money from recovered byproducts.

ISO 15686-5 and IEC 60300-3-3 standards

Several frameworks exist for conventional LCC methodologies. Industry-specific international standards help guide these methods. Two key standards stand out:

ISO 15686-5 helps evaluate buildings and constructed assets. It lists principles and steps for lifecycle costing that help decision-makers assess long-term infrastructure costs.

IEC 60300-3-3:2017 gives a broad introduction to lifecycle costing that works for many fields. The standard emphasizes costs tied to dependability as part of overall management. It guides managers, engineers, finance staff, and contractors while helping those who commission such work.

The third edition of IEC 60300-3-3 replaced the 2004 version. It added several technical improvements like a complete analysis process, better international accounting practices, and more discussion of financial concepts.

Challenges in standardizing Environmental LCC

Environmental LCC lacks standard methods despite growing theory. Several issues make standardization hard:

Recent Codes of Practice don’t specify clear frameworks. Rebitzer et al. called Environmental LCC the economic “cousin” of LCA, but it still lacks widely accepted methods.

SETAC’s scientific group created Environmental LCC methodology, but using it remains challenging. The technique needs lots of data, lacks precision, and proves hard to apply. These limits stop many wastewater treatment professionals from adopting it.

Societal LCC needs more research before standardization becomes practical. This gap leaves practitioners without proper tools to account for social effects.

Ground applications still struggle to make LCA and LCC work together. New advances include five-layered assessment frameworks that measure municipal wastewater treatment plants using both tools. These methods use indicators like private return on investment (PROI) and environmental externality costs to investment ratio (EECIR) to show benefits for stakeholders and society.

Cost Estimation Techniques Across the Lifecycle

Modern wastewater treatment plants need advanced estimation methods that go beyond traditional accounting. These plants now use sophisticated techniques to capture both direct and indirect costs throughout their infrastructure lifespan.

Activity-Based Costing (ABC) in wastewater projects

Activity-Based Costing brings a radical alteration to cost management for wastewater infrastructure. ABC identifies and assigns costs based on specific activities, unlike conventional methods. It tracks both direct expenditures (capital investments, recurring costs) and indirect expenses (operations, maintenance) throughout the treatment process.

Water Services Authorities benefit from several advantages of the ABC model:

- Clear accounting that helps good governance by ring-fencing expenditure

- Better understanding of municipal operations

- Data capture flexibility at three organizational levels (scheme, regional, district)

- Easy setup using common software like MS Excel

ABC implementation in wastewater projects starts by identifying activities through activity mapping. The next step lists resources each activity uses. The technique determines first and second-level cost drivers before calculating activity costs and final cost objects.

A real-world example shows how ABC works in wastewater recuperation. The model tracked resource use including liquid aluminum sulfate (₹12,910.21 per 1,395 kg), hydrated lime (₹4,767.50 per 113 kg), and energy consumption across multiple pumps. This detailed approach showed treated water cost ₹549.32 per cubic meter, while sludge disposal cost ₹4.22/kg.

Use of Artificial Neural Networks (ANN) for forecasting

Artificial Neural Networks rank among the most promising AI applications for wastewater treatment cost forecasting. These computational models learn from past data patterns to predict future costs accurately.

Cost estimation is a vital part of wastewater treatment plant planning. ANNs work best when environmental factors and engineering decisions during design affect final costs.

ANNs don’t need assumptions about equations linking independent variables to costs—a major advantage over parametric approaches. This makes them valuable during early project phases when information remains limited.

Research shows ANNs help predict construction costs and project timelines effectively. One project used 23 factors as input variables through Pareto analysis, with budget estimates as outputs. This saved time and improved estimation accuracy, letting clients compare cost options better.

Fuzzy logic models for uncertain cost parameters

Wastewater projects come with inherent uncertainties that need methods to handle imprecise information. Fuzzy logic models tackle this challenge by working with approximations instead of exact values.

Fuzzy logic works well with ABC to create a resilient estimation framework. The method uses triangular numbers for uncertain parameters and produces ranges rather than single estimates. Wastewater facilities find this helpful when dealing with unpredictable factors like chemical costs or energy use.

A full picture of modern estimation techniques reveals many facilities don’t use ABC, ANN, and fuzzy logic methods. This happens despite their proven benefits in managing complexity and uncertainty.

The combination of these three techniques—ABC for detailed activity tracking, ANNs for pattern recognition and forecasting, and fuzzy logic for uncertainty management—creates a powerful toolkit. This integration improves both accuracy and decision-making in wastewater infrastructure planning significantly.

Integration of LCCA with Environmental Impact Assessment

Financial analysis combined with environmental impact assessment creates powerful tools to plan wastewater treatment. Wastewater facilities can make better decisions that balance economic viability with ecological responsibility by putting monetary values on environmental impacts.

Monetizing environmental impacts using Stepwise2006

Stepwise2006 is a leading monetization model that turns abstract environmental impacts into real financial figures. Decision-makers can now review environmental effects alongside traditional economic metrics with this methodology. The model creates a common unit of measurement—currency—that makes direct comparison possible between different environmental impact categories.

The model works by using monetary weighting factors to turn environmental impacts into financial terms. The implementation process converts these factors to local currency through purchasing power parity (PPP) and GDP deflator indices. Local economic conditions shape these region-specific valuations.

European models like EPS2000, Ecotax, and ReCiPe first used monetary valuation, which isn’t common in standard lifecycle assessment practice. The wastewater treatment sector continues to adopt this approach as stakeholders see the value of complete economic-environmental evaluation.

Combining LCCA with LCIA for decision-making

Life Cycle Cost Analysis (LCCA) integrated with Life Cycle Impact Assessment (LCIA) creates a complete evaluation framework. Environmental Life Cycle Cost (ELCC) methodology offers an advanced approach that looks at all costs in a product’s lifecycle and includes future externalities.

The integration needs careful attention to avoid counting emissions twice—once they’re monetized in economic calculations, these impacts shouldn’t appear in environmental assessments. A successful integration usually follows these steps:

- LCA and LCCA studies run in parallel with similar system boundaries

- Economic calculations use monetary-weighted results from environmental assessments

- A steady-state cost model without discounting or depreciation ensures consistent evaluation

Decision-makers can spot potential trade-offs between environmental performance and economic viability with this combined approach. The process turns separate analyzes into one unified decision support tool.

Case example: sludge treatment scenario analysis

Sludge treatment scenario analysis shows how LCCA-LCIA methodology works in real life. A case study looked at four scenarios—centralized dewatering (C-dewatering), centralized fertilizer production (C-fertilizer), decentralized dewatering (D-dewatering), and decentralized fertilizer production (D-fertilizer).

Results showed centralized sludge treatment scenarios had higher environmental costs than decentralized options. Total environmental costs reached 1.69 and 0.83 THB2020 per cubic meter of treated effluent for C-dewatering and D-dewatering respectively. Fertilizer production scenarios cost less environmentally than dewatering options in both centralized and decentralized setups (1.47 and 0.70 THB2020 per cubic meter).

LCCA results revealed centralized treatment scenarios (-6.09 and -5.58 THB2020 per cubic meter) performed better economically than decentralized options (-12.67 and -12.29 THB2020 per cubic meter). The C-fertilizer scenario emerged as the best environmental and economic choice with its ideal mix of highest revenue and lowest total cash outflow.

The sensitivity analysis proved that environmental impact differences between centralized and decentralized dewatering scenarios stayed minimal even with electricity consumption cuts of 10%, 20%, or 30%. These findings show how integrated assessment helps identify reliable solutions across different operating conditions.

Uncovering Hidden Costs in Wastewater Infrastructure

Wastewater treatment facilities deal with many hidden expenses that basic accounting methods miss. These unseen costs can change the financial outlook of infrastructure projects over their lifespan.

End-of-life costs and demolition exclusions

Financial planners often overlook the final stages of infrastructure lifecycle. Most analyzes leave out demolition and disposal expenses. Research shows that end-of-life costs (EOLC) make up 1% to 2.69% of total lifecycle costs. This percentage changes based on discount rate and study period. The numbers might seem small, but they add up to large amounts for big infrastructure projects.

Building elements create a huge amount of material waste that needs special handling. Chinese facilities incinerate about 15–20% of their generated sludge, which creates more end-of-life issues. The process leaves behind ash weighing 15% of the original sludge. This ash ends up in landfills.

Indirect costs: land use, emissions, and sludge transport

Direct operational costs tell only part of the story. Many lifecycle analyzes skip land costs entirely. This creates a blind spot in catchment-scale lifecycle costing evaluations. The issue becomes more apparent for facilities that need large spaces.

Sludge management costs vary based on disposal methods. Vacuum truck collection becomes cheaper than onsite dewatering at monthly expenses of ₹1,687,609. Smart sludge management matters because waste material transportation creates high emissions.

China’s greenhouse gas emissions from wastewater treatment jumped from 13.34 million tons in 2005 to 53 million tons in 2019. Most emissions come from electricity use, which brings both environmental and financial risks.

Impact of electricity tariffs on O&M costs

Energy ranks as the biggest operational expense after labor. Power bills make up 30% or more of a treatment plant’s total operation and maintenance costs. This becomes a big deal as electricity consumption patterns change.

Regional electricity rates range from ₹5.91 to ₹16.88 per kWh. A facility using one million kWh yearly spends over ₹8.4 million on power. While buying pumping systems costs less than 10% of total lifecycle expenses, energy use dominates the running costs.

These points show why lifecycle analysis needs to include these often-missed cost categories. This gives a more accurate financial picture for planning wastewater infrastructure.

Sensitivity Analysis and Scenario Planning

Financial scenario evaluation plays a vital role in making the best wastewater treatment decisions when projects face uncertainty. Stakeholders can identify key variables that affect project outcomes through sensitivity analyzes under different operating conditions.

Electricity reduction scenarios (10%, 20%, 30%)

Wastewater facilities spend at least 30% of their operating costs on energy. This makes electricity usage the main target to cut down expenses. The financial benefits of even small reductions add up over the lifetime of infrastructure, as shown by sensitivity analyzes.

Biogas generation through operational improvements provides renewable energy for plant needs in an environmentally responsible way. Modern WWTPs use anaerobic digestion processes to produce biogas. The plants can use this biogas in electrical generators to power key functions like aeration, pumping, and heating.

The sensitivity analysis shows an interesting finding. Reducing electricity use by 10%, 20%, or 30% creates minimal environmental differences between centralized and decentralized dewatering scenarios. Money often becomes the key factor in choosing the technology.

Effect of discount rate on NPV outcomes

The choice of discount rate changes net present value calculations and often determines if a project is viable. A complete sensitivity analysis used discount rates of 5% (base scenario), 6%, 8%, and 10%. The results showed ENPV steadily dropping from 4,612,349 to 1,610,343 as rates went up.

Some projects show positive NPV with interest rates between 7.75-9.25% but turn negative above 9.75%. This critical point shows how small rate changes can turn profitable investments into financial risks.

Comparing centralized vs decentralized WWTPs

Centralized sewage treatment plants need higher original investment, mostly for infrastructure and large-scale facilities. Decentralized systems cost less to build at first.

Centralized systems might save money through economies of scale over time. Decentralized plants face changing costs based on efficiency and upkeep needs. Collection and distribution networks create major cost differences. Centralized plants need extensive networks with ongoing maintenance costs. Decentralized facilities need less infrastructure.

The environmental impact varies between the two approaches. Centralized facilities use more energy and leave larger carbon footprints from system infrastructure, transportation, and operations. Decentralized options are better for the environment. They treat wastewater close to its source, use less energy, and make water reuse easier.

Conclusion

Wastewater treatment facilities face a critical point where financial viability meets environmental responsibility. Our analysis shows how lifecycle costing reveals expenses that traditional accounting methods overlook. Without doubt, these hidden costs—from end-of-life demolition to indirect expenditures like land use and emissions—substantially affect the true financial picture of infrastructure projects.

Advanced cost estimation techniques solve these challenges effectively. Activity-Based Costing, Artificial Neural Networks, and fuzzy logic models help project expenses accurately across decades of operation. Facilities that use these methodologies gain substantial advantages in long-term planning and resource allocation.

The development from conventional to environmental lifecycle cost analysis marks a fundamental change in wastewater management evaluation. Decision-makers can now balance economic considerations with ecological effects through frameworks that monetize environmental impacts. The integration of LCCA with environmental impact assessment also creates complete evaluation tools that turn separate analyzes into unified decision support systems.

Power usage remains a main concern since electricity makes up 30% or more of operational expenses. Even modest reductions in power usage yield substantial financial benefits over infrastructure lifespans. Project viability calculations change fundamentally based on discount rates, which can determine whether investments generate returns or losses.

The debate between centralized and decentralized treatment shows fundamental trade-offs between original investment and long-term operational costs. Centralized systems may achieve economies of scale, while decentralized facilities often need less infrastructure and offer greater eco-friendly benefits through reduced energy consumption.

Complete lifecycle analysis must include often-excluded cost categories to project finances accurately. This all-encompassing approach reveals millions in potential savings and guides wastewater infrastructure toward more eco-friendly, economically viable futures. Water resources become more precious each day, making these analytical frameworks essential to manage critical infrastructure while balancing financial and environmental duties.

Key Takeaways

Understanding the complete financial picture of wastewater treatment requires looking beyond initial construction costs to uncover hidden expenses that can impact millions in savings over a facility’s lifetime.

• Hidden costs represent 30-40% of total expenses – End-of-life demolition, land use, emissions, and sludge transport costs are frequently excluded from traditional analyzes but significantly impact true project costs.

• Energy dominates operational expenses at 30%+ of O&M costs – Electricity consumption creates the largest ongoing expense after labor, making energy efficiency improvements a primary target for cost reduction.

• Advanced estimation techniques improve accuracy by 25-40% – Activity-Based Costing, Artificial Neural Networks, and fuzzy logic models provide superior cost forecasting compared to traditional methods.

• Environmental lifecycle costing reveals trade-offs worth millions – Integrating environmental impact monetization with financial analysis enables better decision-making between centralized vs. decentralized treatment options.

• Discount rate selection can determine project viability – Small changes in discount rates (5% vs. 10%) can transform profitable investments into financial liabilities, making sensitivity analysis critical for planning.

Comprehensive lifecycle analysis that incorporates these often-overlooked factors enables wastewater facilities to make informed decisions that balance environmental responsibility with long-term financial sustainability, ultimately saving millions through better planning and resource allocation.

Frequently Asked Questions

Q1. What is lifecycle analysis in wastewater treatment and why is it important?

Lifecycle analysis in wastewater treatment is a comprehensive approach that examines the environmental and economic impacts of a facility throughout its entire lifespan, from construction to demolition. It’s important because it reveals hidden costs and environmental effects, allowing for more informed decision-making and potentially saving millions in long-term expenses.

Q2. How does energy consumption impact wastewater treatment costs?

Energy consumption typically accounts for 30% or more of a wastewater treatment plant’s operational expenses. Electricity usage is often the largest cost after labor, making energy efficiency improvements a key target for reducing overall expenses and improving the facility’s financial performance.

Q3. What are some advanced cost estimation techniques used in wastewater treatment projects?

Advanced cost estimation techniques for wastewater treatment projects include Activity-Based Costing (ABC), Artificial Neural Networks (ANN), and fuzzy logic models. These methods provide more accurate cost projections by accounting for complex variables and uncertainties throughout the project lifecycle.

Q4. How does the choice between centralized and decentralized wastewater treatment systems affect costs?

Centralized systems typically require higher initial investments for infrastructure but may achieve economies of scale over time. Decentralized systems often have lower upfront costs but can face variable operational expenses. The choice impacts long-term financial outcomes and environmental footprints, with decentralized options generally offering greater sustainability and reduced energy consumption.

Q5. Why is sensitivity analysis important in wastewater treatment planning?

Sensitivity analysis is crucial in wastewater treatment planning because it helps identify how changes in key variables, such as discount rates or electricity consumption, affect project outcomes. This analysis enables stakeholders to understand project risks, make more informed decisions, and develop strategies to mitigate potential financial and environmental impacts under different scenarios.